What Is Financial Technology (Fintech)

Fintech, short for financial technology, refers to the innovative use of technology to design and deliver financial services. It covers a wide range of applications including digital payments, online banking, blockchain, cryptocurrencies, and more. FinTech aims to improve and automate the delivery and use of financial services, making these services more convenient, efficient and user-friendly. By leveraging the latest technologies, fintech companies can offer cutting-edge financial solutions that traditional banking systems cannot provide

Financial technology, commonly known as fintech, refers to advanced technology that aims to improve and automate financial services. At its core, financial technology helps businesses, business owners and consumers manage their financial activities more efficiently. This is achieved thanks to special programs and algorithms used on computers and smartphones. The term “Fintech” is a combination of the words “finance” and “technology”. Social Media Managemnt Free Courses.

Table of Contents

Importance Of Fintech In Todays’s World

In today’s fast-paced, digital-first world, fintech is reshaping the way we interact with money. From transferring money with a few taps on a smartphone to investing in stocks through easy-to-use apps, fintech has revolutionized the financial landscape. It provides greater access to financial services to people around the world, promotes financial inclusion and fosters innovation in the financial sector.

When fintech emerged in the 21st century, it initially referred to the technology used in the back-end systems of existing financial institutions such as banks. However, from around 2018 to 2022, there was a shift towards customer-centric services. Today, fintech spans a variety of sectors and industries, including education, retail banking, fundraising and nonprofits, and investment management, among others.

Main Idea

- FinTech refers to the integration of technology into financial services and improving their use and delivery to consumers. It works primarily by cannibalizing traditional offerings and creating new markets.

- Financial companies using FinTech have increased financial inclusion and reduced operating costs through technology. Although fintech financing is on the rise, regulatory challenges remain.

- Examples of fintech apps include robo-advisors, payment apps, peer-to-peer (P2P) lending apps, investment apps, and cryptocurrency apps.

Heighlights

- The Largest market wiii be Digital Assets with a AUM of US$ 32.54m in 2024.

- The Average AUM per user in the Digital Assets Market is projected to amount to US$ 7.77 in 2024.

- The Digital Assets Market is expected to show a revenue growth of 32.92% in 2025.

- In the Digital Payments Market ,the number of users is expected to amount to 29.710.00k users by 2028.

Understanding Fintech

In general, the term “financial technology” includes any innovation in business transaction procedures, from the creation of digital currency to the development of double-entry bookkeeping. Since the advent of the Internet, financial technology has experienced tremendous growth.

You probably use some type of financial technology every day. Examples include transferring money from your bank account to a checking account on your iPhone, sending money to a friend via Venmo, or managing investments through an online broker. According to the 2019 EY Global FinTech Adoption Index, two-thirds of consumers use at least two fintech services, and these consumers are becoming increasingly aware of fintech in their daily lives.

Fintech In Practice

The most prominent and well-funded fintech startups share a common goal: to challenge traditional financial services providers and ultimately serve underserved sectors by becoming more efficient, more agile, or To provide faster and better services.

Affirm, for example, aims to outpace credit card companies in online shopping by providing consumers with fast, short-term loans to make purchases. Despite the high rates, Avram offers people with poor or no credit a way to secure credit and build their credit history.

Similarly, Better Mortgage simplifies the mortgage process with its digital-only service that can provide a certified pre-approval letter within 24 hours of application. GreenSky connects home improvement borrowers with banks, helping them avoid traditional lenders and save on interest through interest-free promotional periods.

For poor or uncredited consumers, Tala provides microloans to consumers in developing countries by analyzing smartphone data, including seemingly unrelated information such as transaction history and mobile game usage. Tala aims to provide better options than local banks, unorganized lenders and other microfinance institutions.

In short, if you’ve ever wondered why certain aspects of your financial life, like applying for a mortgage with a traditional lender, are so unpleasant or seem so inconvenient, chances are fintech is making it happen (or aiming to). solution for.

Are you wondering how to withdraw money from Hamster Kombat? Have you been mining Hamster Kombat Coins for a long time and are not sure about the withdrawal process? In this case Indogist will explain every aspect of eliminating Hamster Kombat. Those with experience in the cryptocurrency space may be familiar with companies like Hamster Kombat. This platform is an online click game that pays participants with coins after completing certain tasks.On the other hand, one can imagine Hamster Kombat as a tap game on Telegram that allows players to earn coins by tapping the screen and performing tasks. The current question is related to the process of withdrawing coins earned in Hamster Kombat. Fear not, as we walk you through the intricacies of the Hamster Kombat removal process.

Fintech Growing Scope In Pakistan

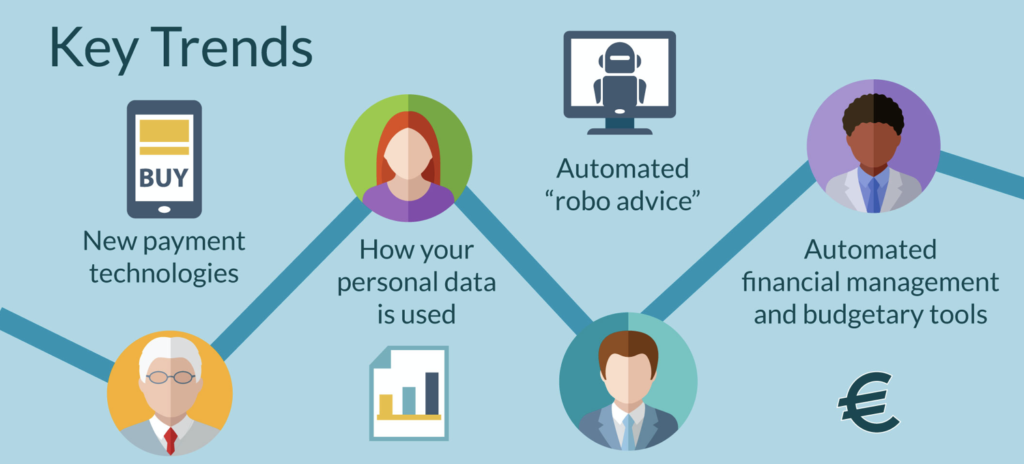

The FinTech sector is developing rapidly, with digital payments, digital investments, digital fundraising, digital assets and new banking emerging as key trends. Digital payments have gained immense popularity as consumers increasingly rely on mobile payment solutions for their daily transactions. Similarly, digital investment platforms that provide individuals with low-cost, easy-to-use investment opportunities are also gaining traction.In addition, digital fundraising has become attractive to startups and SMEs, providing effective access to finance. The emergence of digital assets such as cryptocurrencies and non-fungible tokens (NFTs) has opened new horizons for investors and traders. Neobanks have revolutionized the traditional banking industry by providing innovative, customer-centric solutions to today’s digitally savvy customers.

There are various factors driving the growth of the FinTech market. First, the widespread adoption of smartphones and the Internet has increased demand for fintech services by democratizing access to digital solutions. Second, the COVID-19 pandemic has accelerated the shift to digital payments and investments, pushing consumers to embrace remote and contactless transactions. Third, regulatory changes have leveled the playing field, allowing fintech companies to compete more effectively with traditional financial institutions. Finally, advances in technologies such as artificial intelligence and blockchain have accelerated market expansion by encouraging innovation in financial technology.

The fintech sector is expected to continue its rapid growth trajectory, supported by ongoing technological advancements, consumer preferences and evolving regulatory frameworks. Digital payments are expected to dominate due to consumer demand for convenience and speed in transactions. Digital investment platforms will likely continue to attract more users looking for digital financial management solutions. Additionally, the expansion of digital assets and new banking services is expected to reshape the financial landscape. Overall, the fintech market is expected to remain dynamic and innovative, constantly introducing new services and solutions to meet the changing needs of consumers.

What are Examples of Fintech

Fintech has been applied to many areas of fiance. Here are just few examples;

- Robo-Advisors: These are apps or online platforms that automatically manage your money efficiently, often at a low cost, and are accessible to ordinary people.

- Investment Apps: Platforms like Robinhood simplify the process of buying and selling stocks, exchange-traded funds (ETFs), and cryptocurrencies right from your mobile device, often with little or no commission.

- Payments Apps : Services like PayPal, Venmo, Square’s Cash App, Zelle, and Block allow individuals or businesses to process payments online quickly and easily.

- Personal Finance Apps:Tools like Mint, YNAB (You Need a Budget), and Quicken Simplifi let you manage all your money in one place, set a budget, pay bills, and more.

- Peer-2-Peer lending: Platforms like Prosper Marketplace, LendingClub, and Upstart allow individuals and small business owners to borrow directly from a variety of lenders who provide them with microloans.

- Crypto Apps:These platforms, including wallets, exchanges, and payment apps, allow you to store and execute transactions on cryptocurrencies, digital tokens like bitcoin, and non-fungible tokens (NFTs).

FAQ’s

Does Fintech apply only to banking?

No, While banks and startups are developing fintech applications useful for core banking services like current and savings accounts, bank transfers, credit/debit cards, and loans, various fintech segments related to personal finance, investments, payments, etc. have seen a rise in Its popularity. . And more.

Is Fintech in demand?

The FinTech sector is growing rapidly globally, driven by growing consumer demand. Fintech particularly benefits business owners, small businesses and isolated communities, according to Brian Chang of the Cambridge Center for Alternative Finance.

1 thought on “07 What Is Fintech, Its Growing Scope In Pakistan”